UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D. C. 20549

__________________________________________________________________________________________________________________________

FORM 10‑K |

| |

☒ | Annual Report Pursuant to Section 13 of 15(d) of the Securities Exchange Act of 1934 |

For the Fiscal Year Ended September 30, 2017

or

|

| |

☐ | Transition Report Pursuant To Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the Transition Period from _____ to _____

Commission File No. 0‑09115

__________________________________________________________________________________________________________________________

MATTHEWS INTERNATIONAL CORPORATION

(Exact name of registrant as specified in its charter)

|

| | |

PENNSYLVANIA | | 25‑0644320 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

| | |

TWO NORTHSHORE CENTER, PITTSBURGH, PA | | 15212‑5851 |

(Address of principal executive offices) | | (Zip Code) |

(412) 442-8200 |

(Registrant's telephone number, including area code) |

Securities registered pursuant to Section 12(b) of the Act: |

Title of each class | | Name of each exchange on which registered |

Class A Common Stock, $1.00 par value | | Nasdaq Global Select Market |

| | |

Securities registered pursuant to Section 12(g) of the Act: None |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

|

| | | | |

Large accelerated filer | ☒ | | Smaller reporting company | ☐ |

Accelerated filer | ☐ | | Emerging growth company | ☐ |

Non-accelerated filer | ☐ | (Do not check if a smaller reporting company) | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No ☒

The aggregate market value of the Class A Common Stock held by non-affiliates of the registrant, based upon the closing sale price of the Class A Common Stock on the Nasdaq Global Select Market on March 31, 2017, the last business day of the registrant's most recently completed second fiscal quarter, was approximately $2.1 billion.

As of October 31, 2017, shares of common stock outstanding were: Class A Common Stock 32,148,579 shares.

Documents incorporated by reference: Specified portions of the Proxy Statement for the 2018 Annual Meeting of Shareholders are incorporated by reference into Part III of this Report.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING INFORMATION:

Any forward-looking statements contained in this Annual Report on Form 10-K (specifically those contained in Item 1, "Business," Item 1A, "Risk Factors" and Item 7, "Management's Discussion and Analysis of Financial Condition and Results of Operations") are included in this report pursuant to the "safe harbor" provisions of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements involve known and unknown risks and uncertainties that may cause the actual results of Matthews International Corporation ("Matthews" or the "Company") in future periods to be materially different from management's expectations. Although the Company believes that the expectations reflected in such forward-looking statements are reasonable, no assurance can be given that such expectations will prove correct. In addition to the risk factors previously disclosed and those discussed elsewhere in this Annual Report on Form 10-K, factors that could cause the Company's results to differ materially from the results discussed in such forward-looking statements principally include changes in domestic or international economic conditions, changes in foreign currency exchange rates, changes in the cost of materials used in the manufacture of the Company's products, changes in mortality and cremation rates, changes in product demand or pricing as a result of consolidation in the industries in which the Company operates, changes in product demand or pricing as a result of domestic or international competitive pressures, unknown risks in connection with the Company's acquisitions, cybersecurity concerns, effectiveness of the Company's internal controls, compliance with domestic and foreign laws and regulations, technological factors beyond the Company's control, and other factors described in Item 1A, "Risk Factors" in this Form 10-K. In addition, although the Company does not have any customers that would be considered individually significant to consolidated sales, changes in the distribution of the Company's products or the potential loss of one or more of the Company's larger customers are also considered risk factors.

ITEM 1. BUSINESS.

Matthews, founded in 1850 and incorporated in Pennsylvania in 1902, is a provider principally of brand solutions, memorialization products and industrial technologies. Brand solutions include brand development, deployment and delivery (consisting of brand management, pre-media services, printing plates and cylinders, and imaging services for consumer packaged goods and retail customers, merchandising display systems, and marketing and design services). Memorialization products consist primarily of bronze and granite memorials and other memorialization products, caskets and cremation equipment primarily for the cemetery and funeral home industries. Industrial technologies include marking and coding equipment and consumables, industrial automation solutions and order fulfillment systems for identifying, tracking, picking and conveying consumer and industrial products.

At October 31, 2017, the Company and its majority-owned subsidiaries had approximately 11,000 employees. The Company's principal executive offices are located at Two NorthShore Center, Pittsburgh, Pennsylvania 15212, its telephone number is (412) 442-8200 and its website is www.matw.com. The Company files or furnishes all required reports with the Securities and Exchange Commission ("SEC") in accordance with the Exchange Act. The Company's Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports are available free of charge on the Company's website as soon as reasonably practicable after being filed or furnished to the SEC. The Company's reports filed or furnished with the SEC, including exhibits attached to such reports, are also available to read and copy at the SEC's Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549 or by contacting the SEC at 1-800-732-0330. All Company reports filed with or furnished to the SEC can be found on its website at www.sec.gov.

The Company has three reporting segments, SGK Brand Solutions, Memorialization, and Industrial Technologies. The following table sets forth reported sales and operating profit for the Company's business segments for the past three fiscal years. Detailed financial information relating to business segments and to domestic and international operations is presented in Note 18, "Segment Information" in Item 8 - "Financial Statements and Supplemental Data."

ITEM 1. BUSINESS, (continued)

|

| | | | | | | | | | | |

| Years Ended September 30, |

| 2017 | | 2016 | | 2015 |

| (Amounts in thousands) |

Sales to unaffiliated customers: | | | | | |

SGK Brand Solutions | $ | 770,181 |

| | $ | 755,975 |

| | $ | 798,339 |

|

Memorialization | 615,882 |

| | 610,142 |

| | 508,058 |

|

Industrial Technologies | 129,545 |

| | 114,347 |

| | 119,671 |

|

Consolidated | $ | 1,515,608 |

| | $ | 1,480,464 |

| | $ | 1,426,068 |

|

Operating profit: | | | | | |

SGK Brand Solutions | $ | 24,919 |

| | $ | 42,909 |

| | $ | 21,864 |

|

Memorialization | 80,652 |

| | 68,252 |

| | 70,064 |

|

Industrial Technologies | 7,032 |

| | 7,654 |

| | 13,095 |

|

Consolidated | $ | 112,603 |

| | $ | 118,815 |

| | $ | 105,023 |

|

In fiscal 2017, approximately 67% of the Company's sales were made from the United States, 26% were made from Europe, 3% were made from Asia, and 4% were made from other regions. For further information on segments, see Note 18, "Segment Information" in Item 8 - "Financial Statements and Supplementary Data" on page 69 of this Report. Products and services of the SGK Brand Solutions segment are sold throughout the world, with principal locations in the United States, Europe and Asia. Memorialization segment products are sold throughout the world, with the segment's principal operations located in the United States, Europe, Canada, and Australia. The Industrial Technologies segment sells equipment and consumables directly to industrial consumers and distributors in the United States and internationally through the Company's subsidiaries in Canada, Sweden, Germany and China, and through other foreign distributors. Matthews owns a minority interest in Industrial Technologies product distributors in Asia, Australia and Europe.

SGK Brand Solutions:

The SGK Brand Solutions segment provides brand development, deployment and delivery (consisting of brand management, pre-media services, printing plates and cylinders, and imaging services for consumer packaged goods and retail customers, merchandising display systems, and marketing and design services). The Company has extensive product offerings and capabilities related to brand development and brand management, serving the consumer packaged goods and retail industries. The primary packaging industry consists of manufacturers of printed packaging materials such as boxes, flexible packaging, folding cartons and bags commonly displayed at retailers of consumer goods. The corrugated packaging industry consists of manufacturers of printed corrugated containers. Other major industries served include the wallpaper, flooring, automotive, and textile industries.

The principal products and services of this segment include brand development, deployment, delivery, brand management, pre-media graphics services, 3-D graphics renderings, printing plates, gravure cylinders, steel bases, embossing tools, special purpose machinery, engineering assistance, print process assistance, print production management, digital asset management, content management, and package design. These products and services are used by brand owners and packaging manufacturers to develop and print packaging graphics that help identify and sell the product in the marketplace. Other packaging graphics can include nutritional information, directions for product use, consumer warning statements and UPC codes. The primary packaging manufacturer produces printed packaging from paper, film, foil and other composite materials used to display, protect and market the product. The corrugated packaging manufacturer produces printed containers from corrugated sheets. Using the Company's products, these sheets are printed and die cut to make finished containers.

ITEM 1. BUSINESS, (continued)

The segment offers a wide array of value-added services and products. These include print process and print production management services; print engineering consultation; pre-media preparation, which includes computer-generated art, film and proofs; plate mounting accessories and various press aids; and press-side print production assurance. The segment also provides creative digital graphics services to brand owners and packaging markets.

The segment's sales are also derived from the design, engineering, manufacturing and execution of merchandising and display systems. These systems include permanent and temporary displays, custom store fixtures, brand concept shops, interactive media, custom packaging, and screen and digitally printed promotional signage. Design and engineering services include concept and model development, graphics design and prototyping. Merchandising and display systems are manufactured to specifications developed by the segment in collaboration with the customer.

The Company works closely with manufacturers to provide the proper printing forms and tooling required to print the packaging to the user's specifications. The segment's printing plate products are made principally from photopolymer resin and sheet materials. Upon customer request, plates can be pre-mounted press-ready in a variety of configurations that maximize print quality and minimize press set‑up time. Gravure cylinders, manufactured from steel, copper and chrome, can be custom engineered for multiple print processes and specific customer print applications.

The SGK Brand Solutions segment customer base consists primarily of brand owners and packaging industry converters. Brand owners are generally large, well-known consumer products companies and retailers with a national or global presence. These types of companies tend to purchase their graphics needs directly, and supply the printing forms, or the electronic files to make the printing plates and gravure cylinders, to the packaging printer for their products. The SGK Brand Solutions segment serves customers throughout the world, with principal locations in the United States, Europe, Australia and Asia.

Major raw materials for this segment's products include photopolymers, steel, copper, film, wood, particleboard, corrugated materials, structural steel, plastic, laminates, inks and graphic art supplies. All such materials are presently available in adequate supply from various industry sources.

The SGK Brand Solutions segment is one of several providers of brand management, brand development and pre-media services and manufacturers of printing plates and cylinders with an international presence. The combination of the Company's businesses in North America, Europe and Asia is an important part of Matthews' strategy to be a worldwide leader in the graphics industry by providing consistent service to multinational customers on a global basis. Competition is on the basis of product quality, timeliness of delivery and price. The merchandising and display business operates in a fragmented industry consisting primarily of a number of small, locally operated companies. The segment competes on the basis of reliability, creativity and ability to provide a broad array of merchandising products and services. The segment is unique in its ability to provide in-depth marketing and merchandising services as well as design, engineering and manufacturing capabilities. These capabilities allow the segment to deliver complete turnkey merchandising solutions quickly and cost effectively. The Company differentiates itself from the competition by consistently meeting these customer demands, providing service to customers both nationally and globally, and providing a variety of value-added support services.

Memorialization:

The Memorialization segment manufactures and markets a full line of memorialization products used primarily in cemeteries, funeral homes and crematories. The segment's products, which are sold principally in the United States, Europe, Canada and Australia, include cast bronze memorials, granite memorials, caskets, cremation equipment and other memorialization products. The segment also manufactures and markets architectural products that are used to identify or commemorate people, places, events and accomplishments.

ITEM 1. BUSINESS, (continued)

Memorial products include flush bronze and granite memorials, upright granite memorials and monuments, cremation memorialization products, granite benches, flower vases, crypt plates and letters, cremation urns, niche units, cemetery features and statues, along with other related products and services. Flush memorials are bronze plaques or granite memorials which contain personal information about a deceased individual (such as name, birth date, and death date), photos and emblems. Flush bronze and granite memorials are even or "flush" with the ground and therefore are preferred by many cemeteries for easier lawn mowing and general maintenance. The segment's memorial products also include community and family mausoleums within North America. In addition, the segment's other memorial products include bronze plaques, letters, emblems, vases, lights and photo ceramics that can be affixed to granite monuments, mausoleums, crypts and flush memorials. Principal customers for memorial products are cemeteries and memorial parks, which in turn sell the Company's products to the consumer.

Customers of the Memorialization segment can also purchase memorials and vases on a "pre-need" basis. The "pre-need" concept permits families to arrange for these purchases in advance of their actual need. Upon request, the Company will manufacture the memorial to the customer's specifications (e.g., name and birth date) and place it in storage for future delivery. Memorials in storage have been paid in full with title conveyed to each pre-need purchaser.

The segment is also a leading manufacturer and distributor of caskets and other funeral home products in North America. The segment produces and markets metal, wood and cremation caskets. Caskets are offered in a variety of colors, interior designs, handles and trim in order to accommodate specific religious, ethnic or other personal preferences. The segment also markets other funeral home products such as urns, jewelry and stationery. The segment offers individually personalized caskets through its distribution network.

Metal caskets are made from various gauges of cold-rolled steel, stainless steel, copper and bronze. Metal caskets are generally categorized by whether the casket is non-gasketed or gasketed, and by material (i.e., bronze, copper, or steel) and in the case of steel, by the gauge (thickness) of the metal. Wood caskets are primarily manufactured from nine different species of wood. The species of wood used are poplar, pine, ash, oak, pecan, maple, cherry, walnut and mahogany. The Memorialization segment is a leading manufacturer of all-wood constructed caskets, which are manufactured using pegged and dowelled construction, and include no metal parts. Cremation caskets are made primarily from wood or cardboard covered with cloth or veneer. These caskets appeal primarily to cremation consumers, environmentally concerned consumers, and value buyers.

The Memorialization segment also produces casket components. Casket components include stamped metal parts, metal locking mechanisms for gasketed metal caskets, adjustable beds and interior panels. Metal casket parts are produced by stamping cold-rolled steel, stainless steel, copper and bronze sheets into casket body parts. Locking mechanisms and adjustable beds are produced by stamping and assembling a variety of steel parts. The segment purchases from sawmills and lumber distributors various species of uncured wood, which it dries and cures. The cured wood is processed into casket components.

In addition, the segment provides product and service assortment planning, as well as merchandising and display products to funeral service businesses. These products assist funeral service professionals in providing information, value and satisfaction to their client families.

The segment also provides cremation systems, crematory management, cremation service and supplies, waste management and incineration systems, and environmental and energy solutions to the human, pet and specialized incineration markets. The primary market areas for these products and services are North America and Europe, although the segment also sells into Latin America and the Caribbean, Australia, the Middle East and Asia.

ITEM 1. BUSINESS, (continued)

Cremation systems include flame-based systems for cremation of humans and pets, as well as equipment for processing the cremated remains and other related equipment (ventilated work stations, tables, cooler racks, vacuums). The principal markets for these products are funeral homes, cemeteries, crematories, pet crematories, animal disposers and veterinarians. These products primarily are marketed directly by segment personnel. Human crematory management/operations represent the actual operation and management of client-owned crematories. Currently the segment provides these services primarily to municipalities in Europe and private operators in the United States. Cremation service and supplies consist of operator training, preventative maintenance and "at need" service work performed on various makes and models of equipment. This work can be as simple as replacing defective bulbs or as complex as complete reconstruction and upgrading or retro-fitting on site. Supplies are consumable items associated with normal operations.

Waste management/incineration systems encompass both batch load and continuous feed, static and rotary systems for incineration of all waste types, as well as equipment for in-loading waste, out-loading ash and energy recovery. The principal markets for these products are medical waste disposal, oil and gas "work camp" wastes, industrial wastes and bio-mass generators. Environmental and energy systems include emissions filtration units, waste heat recovery equipment, waste gas treatment products, as well as energy recovery. The principal markets are municipalities or public/state agencies, the cremation industry and other industries which utilize incinerators for waste reduction and energy production.

The Memorialization segment also manufactures a full line of other products, including urns in a variety of sizes, styles and shapes as well as standard and custom designed granite cremation pedestals and benches. The segment manufactures bronze and granite niche units, which are comprised of numerous compartments used to display cremation urns in mausoleums and churches. The Company also markets turnkey cremation gardens, which include the design and all related products for a cremation memorial garden.

Architectural products include cast bronze and aluminum plaques, etchings and letters that are used to recognize, commemorate and identify people, places, events and accomplishments. The Company's plaques are frequently used to identify the name of a building or the names of companies or individuals located within a building. Such products are also used to commemorate events or accomplishments, such as military service or financial donations. The principal markets for the segment's architectural products are corporations, fraternal organizations, contractors, churches, hospitals, schools and government agencies. These products are sold to and distributed through a network of independent dealers including sign suppliers, awards and recognition companies, and trophy dealers.

Raw materials used by the Memorialization segment to manufacture memorials consist principally of bronze and aluminum ingot, granite, sheet metal, coating materials, photopolymers and construction materials and are generally available in adequate supply. Ingot is obtained from various North American, European and Australian smelters. The primary materials required for casket manufacturing are cold-rolled steel and lumber. The segment also purchases copper, bronze, stainless steel, particleboard, corrugated materials, paper veneer, cloth, ornamental hardware and coating materials. Purchase orders or supply agreements are typically negotiated with large, integrated steel producers that have demonstrated timely delivery, high quality material and competitive prices. Lumber is purchased from a number of sawmills and lumber distributors. Raw materials used to manufacture cremation and incineration products consist principally of structural steel, sheet metal, electrical components, combustion devices and refractory materials. These are generally available in adequate supply from numerous suppliers.

Competition from other manufacturers of memorial products is on the basis of reputation, product quality, delivery, price, and design availability. The Company believes that its superior quality, broad product lines, innovative designs, delivery capability, customer responsiveness, experienced personnel and consumer-oriented merchandising systems are competitive advantages in its markets. Competition in the mausoleum construction industry includes various construction companies throughout North America and is on the basis of design, quality and price. Competitors in the architectural market are numerous and include companies that manufacture cast and painted signs, plastic materials, sand-blasted wood and other fabricated products.

ITEM 1. BUSINESS, (continued)

The Memorialization segment markets its casket products in the United States through a combination of Company-owned and independent casket distribution facilities. The Company operates approximately 100 distribution centers in the United States. Approximately 85% of the segment's casket products are currently sold through Company-owned distribution centers. The casket business is highly competitive and the Company competes with other manufacturers on the basis of product quality, price, service, design availability and breadth of product line. The Memorialization segment provides a line of casket products that it believes is as comprehensive as any of its major competitors. There are a large number of casket industry participants operating in North America and also a few foreign casket manufacturers, primarily from China, participating in the North American market.

The Company competes with several manufacturers in the cremation and accessory equipment market principally on the basis of product design, quality and price. The Memorialization segment and its three largest global competitors account for a substantial portion of the U.S. and European cremation equipment market.

The Memorialization segment works to provide a total solution to customers that own and operate businesses in both the cemetery and funeral home markets. The Company's memorial and casket products serve the relatively stable casketed and in-ground burial death market, while its memorial products and cremation equipment also serve the growing cremation market.

Industrial Technologies:

The Industrial Technologies segment designs, manufactures and distributes a wide range of marking and coding equipment and consumables, industrial automation solutions, and order fulfillment systems. Manufacturers, suppliers and distributors worldwide rely on Matthews' integrated systems to identify, track, convey and pick their products.

Marking systems range from mechanical marking solutions to microprocessor-based ink-jet printing systems that integrate into a customer's manufacturing, inventory tracking and material handling control systems. The Company manufactures and markets products and systems that employ different marking technologies, including contact printing, indenting, etching, laser and ink-jet printing. Customers frequently use a combination of these methods to achieve an appropriate mark. These technologies apply product information required for identification and traceability, as well as to facilitate inventory and quality control, regulatory compliance and brand name communication.

Fulfillment systems complement the tracking and distribution of a customer's products with automated order fulfillment technologies, motor-driven rollers for product conveyance, and controls for material handling systems. Material handling customers include some of the largest automated assembly and distribution companies in the United States. The Company also

engineers innovative, custom solutions to address specific customer requirements in a variety of industries, including oil exploration and security scanning.

A significant portion of the revenue of the Industrial Technologies segment is attributable to the sale of consumables and replacement parts required by the marking, coding and tracking products sold by Matthews. The Company develops inks, rubber and steel consumables in conjunction with the marking equipment in which they are used, which is critical to ensure ongoing equipment reliability and mark quality.

The principal customers for the Company's marking and fulfillment systems products are manufacturers, suppliers and distributors of durable goods, building products, consumer goods manufacturers (including food and beverage processors) and producers of pharmaceuticals. The Company also serves a wide variety of industrial markets, including metal fabricators, manufacturers of woven and non-woven fabrics, plastic, rubber and automotive products.

A portion of this segment's sales are outside the United States, with distribution sourced through the Company's subsidiaries in Canada, Sweden, Germany and China in addition to other international distributors. The Company owns a minority interest in distributors in Asia, Australia and Europe.

ITEM 1. BUSINESS, (continued)

Major raw materials for this segment's products include precision components, electronics, printing components, tool steels, rubber and chemicals, all of which are presently available in adequate supply from various sources.

Competitors in the marking and fulfillment systems industries are diverse, with some companies offering limited product lines for well-defined specialty markets, while others operate similarly to the Company, offering a broad product line and competing in multiple product markets and countries. Competition for marking and fulfillment systems products is based on product performance, ease of integration into the manufacturing and/or distribution process, service and price. The Company typically competes with specialty companies in specific brand marking solutions and traceability applications. The Company believes that, in general, its Industrial Technologies segment offers one of the broadest lines of products to address a wide variety of marking, coding and industrial automation applications.

PATENTS, TRADEMARKS AND LICENSES:

The Company holds a number of trademarks and in excess of 100 domestic and foreign patents for its products and related technologies. However, the Company believes the loss of any individual or a significant number of patents or trademarks would not have a material impact on consolidated operations or revenues.

BACKLOG:

Because the nature of the Company's SGK Brand Solutions, Memorialization and Industrial Technologies businesses are primarily custom products made to order and services with short lead times, backlogs are not generally material except for roto-gravure engineering projects in the SGK Brand Solutions segment, mausoleums and cremation equipment in the Memorialization segment and industrial automation and order fulfillment systems in the Industrial Technologies segment. Backlogs vary in a range of approximately six to twelve months of sales for roto-gravure engineering projects and mausoleums. Cremation equipment sales backlogs vary in a range of eight to ten months of sales. Backlogs for Industrial Technologies segment sales generally vary in a range of up to six weeks for standard products and twelve weeks for custom systems. The Company's current backlog is expected to be substantially filled in fiscal 2018.

REGULATORY MATTERS:

The Company's operations are subject to various federal, state and local laws and regulations relating to the protection of the environment. The Company is party to various environmental matters which include obligations to investigate and mitigate the effects on the environment of the disposal of certain materials at various operating and non-operating sites. The Company is currently performing environmental assessments and remediation at these sites, as appropriate. Refer to Note 16, "Environmental Matters" in Item 8 - "Financial Statements and Supplementary Data," for further details.

ITEM 1A. RISK FACTORS, (continued)

ITEM 1A. RISK FACTORS.

There are inherent risks and uncertainties associated with the Company's businesses that could adversely affect its operating performance and financial condition. Set forth below are descriptions of those risks and uncertainties that the Company currently believes to be material. Additional risks not currently known or deemed immaterial may also result in adverse effects on the Company.

Changes in Economic Conditions. Generally, changes in domestic and international economic conditions affect the industries in which the Company and its customers and suppliers operate. These changes include changes in the rate of consumption or use of the Company's products due to economic downturns, volatility in currency exchange rates, and changes in raw material prices resulting from supply and/or demand conditions.

Uncertainty about current global economic conditions poses a risk, as consumers and businesses may continue to postpone or cancel spending. Other factors that could influence customer spending include energy costs, conditions in the credit markets, consumer confidence and other factors affecting consumer spending behavior. These and other economic factors could have an effect on demand for the Company's products and services and negatively impact the Company's financial condition and results of operations.

Foreign Operations. The Company conducts business in more than 25 countries around the world, and in fiscal 2017 approximately 33% of the Company's sales to external customers were to customers outside the United States. In addition, the Company's manufacturing operations, suppliers and employees are located in many places around the world. As such, the Company's future success depends in part on its ability to grow sales in non-U.S. markets. Sales and operations outside of the United States are subject to certain inherent risks, including fluctuations in the value of the U.S. dollar relative to foreign currencies, global economic uncertainties, tariffs, quotas, taxes and other market barriers, political and economic instability, restrictions on the export or import of technology, potentially limited intellectual property protection, difficulties in staffing and managing international operations, potentially adverse tax consequences, and required compliance with non-U.S. laws and regulations.

Changes in Foreign Currency Exchange Rates. Manufacturing and sales of a significant portion of the Company's products are outside the United States, and accordingly, the Company holds assets, incurs liabilities, earns revenue and pays expenses in a variety of currencies. The Company's consolidated financial statements are presented in U.S. dollars, and therefore, the Company must translate the reported values of its foreign assets, liabilities, revenue and expenses into U.S. dollars. Increases or decreases in the value of the U.S. dollar compared to foreign currencies may negatively affect the value of these items in the Company's consolidated financial statements, even though their value has not changed in local currency.

Increased Prices for Raw Materials. The Company's profitability is affected by the prices of the raw materials used in the manufacture of its products. These prices may fluctuate based on a number of factors, including changes in supply and demand, domestic and global economic conditions, volatility in commodity markets, currency exchange rates, labor costs and fuel-related costs. If suppliers increase the price of critical raw materials, alternative sources of supply, or alternative materials, may not exist or be readily available.

The Company has standard selling price structures (i.e., list prices) in certain of its segments, which are reviewed for adjustment generally on an annual basis. In addition, the Company has established pricing terms with several of its customers through contracts or similar arrangements. Based on competitive market conditions and to the extent that the Company has established pricing terms with customers, the Company's ability to immediately increase the price of its products to offset the increased costs may be limited. Significant raw material price increases that cannot be mitigated by selling price increases or productivity improvements will negatively affect the Company's results of operations.

ITEM 1A. RISK FACTORS, (continued)

Changes in Mortality and Cremation Rates. Generally, life expectancy in the United States and other countries in which the Company's Memorialization segment operates has increased steadily for several decades and is expected to continue to do so in the future. The increase in life expectancy is also expected to impact the number of deaths in the future. Additionally, cremations have steadily grown as a percentage of total deaths in the United States since the 1960's, and are expected to continue to increase in the future. The Company expects that these trends will continue in the future and sales of the Company's Memorialization segment may benefit from the continued growth in the number of cremations; however, such trends may adversely affect the volume of bronze and granite memorialization products and burial caskets sold in the United States.

Changes in Product Demand or Pricing. The Company's businesses have and will continue to operate in competitive markets. Changes in product demand or pricing are affected by domestic and foreign competition and an increase in consolidated purchasing by large customers operating in both domestic and global markets. The Memorialization businesses generally operate in markets with ample supply capacity and demand which is correlated to death rates. The Brand Solutions businesses serve global customers

that are requiring their suppliers to be global in scope and price-competitive. Additionally, in recent years the Company has witnessed an increase in products manufactured offshore, primarily in China, and imported into the Company's U.S. markets. It is expected that these trends will continue and may affect the Company's future results of operations.

Changes in the Distribution of the Company's Products or the Loss of a Large Customer. Although the Company does not have any customer that is individually significant to consolidated sales, it does have contracts with several large customers in both the Memorialization and SGK Brand Solutions segments. While these contracts provide important access to large purchasers of the Company's products, they can obligate the Company to sell products at contracted prices for extended periods of time. Additionally, any significant divestiture of business properties or operations by current customers could result in a loss of business if the Company is not able to maintain the business with the subsequent owners of the businesses.

Risks in Connection with Acquisitions. The Company has grown in part through acquisitions, and continues to evaluate acquisition opportunities that have the potential to support and strengthen its businesses. There is no assurance however that future acquisition opportunities will arise, or that if they do, that they will be consummated. In addition, acquisitions involve inherent risks that the businesses acquired will not perform in accordance with expectations, or that synergies expected from the integration of the acquisitions will not be achieved as rapidly as expected, if at all. Failure to effectively integrate acquired businesses could prevent the realization of expected rates of return on the acquisition investment and could have a negative effect on the Company's results of operations and financial condition.

Protection of Intellectual Property. Certain of the Company's businesses rely on various intellectual property rights, including patents, copyrights, trademarks and trade secrets, as well as confidentiality provisions and licensing arrangements, to establish proprietary rights. If the Company does not enforce its intellectual property rights successfully, its competitive position may suffer which could harm the Company's operating results. In addition, the Company's patents, copyrights, trademarks and other intellectual property rights may not provide a significant competitive advantage. The Company may need to spend significant resources monitoring its intellectual property rights and may or may not be able to detect infringement by third parties. The Company's competitive position may be harmed if it cannot detect infringement and enforce its intellectual property rights quickly or at all. In some circumstances, the Company may choose to not pursue enforcement because an infringer has a dominant intellectual property position or for other business reasons. In addition, competitors might avoid infringement by designing around the Company's intellectual property rights or by developing non-infringing competing technologies. Intellectual property rights and the Company's ability to enforce them may be unavailable or limited in some countries which could make it easier for competitors to capture market share and could result in lost revenues.

ITEM 1A. RISK FACTORS, (continued)

Environmental Remediation and Compliance. The Company is subject to the risk of environmental liability and limitations on its operations due to environmental laws and regulations. The Company is subject to extensive federal, state, local and foreign environmental, health and safety laws and regulations concerning matters such as air emissions, wastewater discharges, solid and hazardous waste handling and disposal and the investigation and remediation of contamination. The risks of potentially substantial costs and liabilities related to compliance with these laws and regulations are an inherent part of the Company's business, and future conditions may develop, arise or be discovered that create substantial environmental compliance or remediation liabilities and costs. Compliance with environmental, health and safety legislation and regulatory requirements may prove to be more limiting and costly than the Company anticipates, and there is no assurance that significant expenditures related to such compliance may not be required in the future.

From time to time, the Company may be subject to legal proceedings brought by private parties or governmental authorities with respect to environmental matters, including matters involving alleged noncompliance with or liability under environmental, health and safety laws, property damage or personal injury. New laws and regulations, including those which may relate to emissions of greenhouse gases, stricter enforcement of existing laws and regulations, the discovery of previously unknown contamination or the imposition of new clean-up requirements could require the Company to incur costs or become the basis for new or increased liabilities that could have a material adverse effect on the Company's business, financial condition or results of operations.

Technological Factors Beyond the Company's Control. The Company operates in certain markets in which technological product development contributes to its ability to compete effectively. There can be no assurance that the Company will be able to develop new products, that new products can be manufactured and marketed profitably, or that new products will successfully meet the expectations of customers.

Cybersecurity and Data Breaches. In the course of business, the Company collects and stores sensitive data and proprietary business information. The Company could be subject to service outages or breaches of security systems which may result in disruption, unauthorized access, misappropriation, or corruption of this information. Security breaches of the Company's network or data including physical or electronic break-ins, vendor service outages, computer viruses, attacks by hackers or similar breaches can create system disruptions, shutdowns, or unauthorized disclosure of confidential information. Although the Company is not aware of any significant incidents to date, if it is unable to prevent such security or privacy breaches, its operations could be disrupted or the Company may suffer legal claims, loss of reputation, financial loss, property damage, or regulatory penalties because of lost or misappropriated information.

Compliance with Foreign Laws and Regulations. Due to the international scope of the Company's operations, Matthews is subject to a complex system of commercial and trade regulations around the world, and the Company's foreign operations are governed by laws, rules and business practices that often differ from those of the United States. The Company cannot predict the nature, scope or effect of future regulatory requirements to which the Company's operations might be subject or the manner in which existing laws might be administered or interpreted, which could have a material and negative impact on the Company's business and results of operation. For example, recent years have seen an increase in the development and enforcement of laws regarding trade compliance and anti-corruption, such as the U.S. Foreign Corrupt Practices Act and similar laws in other countries. While Matthews maintains a variety of internal policies and controls and takes steps, including periodic training and internal audits, that the Company believes are reasonably calculated to discourage, prevent and detect violations of such laws, the Company cannot guarantee that such actions will be effective or that individual employees will not engage in inappropriate behavior in contravention of the Company's policies and instructions. Such conduct, or even the allegation thereof, could result in costly investigations and the imposition of severe criminal or civil sanctions, could disrupt the Company's business, and could materially and adversely affect the Company's reputation, business and results of operations or financial condition.

ITEM 1A. RISK FACTORS, (continued)

Further, the Company is subject to laws and regulations worldwide affecting its operations outside the United States in areas including, but not limited to, intellectual property ownership and infringement, tax, customs, import and export requirements, anti-corruption and anti-bribery, foreign exchange controls and cash repatriation restrictions, foreign investment, data privacy requirements, anti-competition, pensions and social insurance, employment, and environment, health, and safety. Compliance with these laws and regulations may be onerous and expensive and requirements may differ among jurisdictions. Further, the promulgation of new laws, changes in existing laws and abrogation of local regulations by national laws may have a negative impact on the Company's business and prospects. In addition, certain laws and regulations are relatively new and their interpretation and enforcement involve significant uncertainties. There can be no assurance that any of these factors will not have a material adverse effect on the Company's business, results of operations or financial condition.

Effectiveness of Internal Controls. Section 404 of the Sarbanes-Oxley Act of 2002 requires a comprehensive evaluation of the Company's internal control over financial reporting. To comply with this statute, the Company is required to document and test its internal control over financial reporting, management is required to assess and issue a report concerning internal control over financial reporting, and the Company's independent registered public accounting firm is required to attest to and report on the Company's assessment of the effectiveness of internal control over financial reporting. Any failure to maintain or implement required new or improved controls could cause the Company to fail to meet its periodic reporting obligations or result in material misstatements in the consolidated financial statements, and substantial costs and resources may be required to rectify these or other internal control deficiencies. If the Company cannot produce reliable financial reports, investors could lose confidence in the Company's reported financial information, the market price of the Company's common stock could decline significantly, and its business, financial condition, and reputation could be harmed.

Compliance with Securities Laws and Regulations; Conflict Minerals Reporting. The Company is required to comply with various securities laws and regulations, including but not limited to the Sarbanes-Oxley Act of 2002 and the Dodd-Frank Wall Street Reform and Consumer Protection Act ("Dodd-Frank"). Dodd-Frank contains provisions, among others, designed to improve transparency and accountability concerning the supply chains of certain minerals originating from the Democratic Republic of Congo and adjoining countries that are believed to be benefiting armed groups ("Conflict Minerals"). While Dodd-Frank does not prohibit companies from using Conflict Minerals, the SEC mandates due diligence, disclosure and reporting requirements for companies for which Conflict Minerals are necessary to the functionality or production of a product. The Company's efforts to comply with Dodd-Frank and other evolving laws, regulations and standards could result in increased costs and expenses related to compliance and potential violations.

ITEM 1B. UNRESOLVED STAFF COMMENTS.

Not Applicable.

ITEM 2. PROPERTIES, (continued)

ITEM 2. PROPERTIES.

Principal properties of the Company and its majority-owned subsidiaries as of October 31, 2017 were as follows (properties are owned by the Company except as noted):

|

| | | |

Location | | Description of Property | |

| | | |

SGK Brand Solutions: | | | |

Antwerp, Belgium | | Manufacturing | |

Chennai, India | | Operating facility | (1) |

Chicago, IL | | Operating facilities | (1) |

Cincinnati, OH | | Operating facility | (1) |

Cleckheaton, England | | Operating facility | (1) |

Des Plaines, IL | | Operating facility | (1) |

Dachnow, Poland | | Manufacturing | |

Gateshead, England | | Operating facility | (1) |

East Butler, PA | | Manufacturing | |

Goslar, Germany | | Manufacturing | (1) |

Grenzach-Wyhlen, Germany | | Manufacturing | |

Istanbul, Turkey | | Manufacturing | (1) |

Izmir, Turkey | | Manufacturing | |

Julich, Germany | | Manufacturing | |

Kalamazoo, MI | | Operating facility | |

Kempen, Germany | | Manufacturing | (1) |

Kowloon, Hong Kong | | Operating facility | (1) |

London, England | | Operating facility | (1) |

Manchester, England | | Manufacturing | (1) |

Marietta, GA | | Manufacturing | |

Minneapolis, MN | | Operating facility | |

Mississauga, Canada | | Operating facility | (1) |

Monchengladbach, Germany | | Manufacturing | |

Monchengladbach, Germany | | Manufacturing | (1) |

Munich, Germany | | Manufacturing | (1) |

New Berlin, WI | | Manufacturing | (1) |

Novgorod, Russia | | Manufacturing | |

Nuremberg, Germany | | Manufacturing | (1) |

Penang, Malaysia | | Operating facility | |

Portland, OR | | Operating facility | (1) |

Queretaro, Mexico | | Operating facility | |

Redmond, WA | | Operating facility | (1) |

St. Louis, MO | | Manufacturing | |

San Francisco, CA | | Operating facility | (1) |

Shanghai, China | | Operating facilities | (1) |

Shenzhen, China | | Operating facility | (1) |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

ITEM 2. PROPERTIES, (continued)

|

| | | |

Location | | Description of Property | |

| | | |

SGK Brand Solutions, (continued): | | | |

Tarnowo Podgorne, Poland | | Manufacturing | (1) |

Vreden, Germany | | Manufacturing | |

Vreden, Germany | | Operating facility | |

Wilsonville, OR | | Operating facility | (1) |

| | | |

Memorialization (2): | | | |

Pittsburgh, PA | | Manufacturing / Division Offices | |

Pittsburgh, PA | | Division Offices | (1) |

Apopka, FL | | Manufacturing / Division Offices | |

Apopka, FL | | Operating facility | |

Aurora, IN | | Manufacturing | |

Bristol, TN | | Distribution | |

Colorno, Italy | | Manufacturing | (1) |

Dallas, TX | | Distribution Hub | (1) |

Dandenong, Australia | | Manufacturing | (1) |

Edmunston, Canada | | Manufacturing | |

Elberton, GA | | Manufacturing | (1) |

Fontana, CA | | Distribution Hub | (1) |

Harrisburg, PA | | Distribution Hub | (1) |

Hyde, England | | Manufacturing | (1) |

Indianapolis, IN | | Distribution Hub | (1) |

Kingwood, WV | | Manufacturing | |

Kingwood, WV | | Manufacturing | (1) |

Monterrey, Mexico | | Manufacturing | (1) |

Richmond, IN | | Manufacturing | (1) |

Richmond, IN | | Manufacturing | |

Searcy, AR | | Manufacturing | |

Stone Mountain, GA | | Distribution Hub | (1) |

Udine, Italy | | Manufacturing | (1) |

Vestone, Italy | | Manufacturing | (1) |

West Point, MS | | Distribution | |

Whittier, CA | | Manufacturing | (1) |

York, PA | | Manufacturing | |

| | | |

Industrial Technologies: | | | |

Pittsburgh, PA | | Manufacturing / Division Offices | |

Beijing, China | | Manufacturing | (1) |

Cincinnati, OH | | Manufacturing | (1) |

Cincinnati, OH | | Manufacturing | |

Germantown, WI | | Manufacturing | (1) |

Gothenburg, Sweden | | Manufacturing / Distribution | (1) |

Lima, Costa Rica | | Manufacturing | (1) |

Portland, OR | | Manufacturing | |

Tianjin City, China | | Manufacturing | (1) |

| | | |

| | | |

| | | |

ITEM 2. PROPERTIES, (continued)

|

| | | |

Location | | Description of Property | |

| | | |

Corporate Office: | | | |

Pittsburgh, PA | | General Offices | |

| |

(1) | These properties are leased by the Company under operating lease arrangements. |

| |

(2) | In addition to the properties listed, the Memorialization segment leases warehouse facilities totaling approximately 1.1 million square feet in 38 states under operating leases. |

Rent expense incurred by the Company for all leased facilities was approximately $36.4 million in fiscal 2017.

All of the owned properties are unencumbered. The Company believes its facilities are generally well suited for their respective uses and are of adequate size and design to provide the operating efficiencies necessary for the Company to be competitive. The Company's facilities provide adequate space for meeting its near-term production requirements and have availability for additional capacity. The Company intends to continue to expand and modernize its facilities as necessary to meet the demand for its products.

ITEM 3. LEGAL PROCEEDINGS.

Matthews is subject to various legal proceedings and claims arising in the ordinary course of business. Management does not expect that the results of any of these legal proceedings will have a material adverse effect on Matthews' financial condition, results of operations or cash flows.

ITEM 4. MINE SAFETY DISCLOSURES.

Not applicable.

OFFICERS AND EXECUTIVE MANAGEMENT OF THE REGISTRANT

The following information is furnished with respect to officers and executive management as of October 31, 2017:

|

| | | | |

Name | | Age | | Positions with Registrant |

Joseph C. Bartolacci | | 57 | | President and Chief Executive Officer |

Gregory S. Babe | | 59 | | Chief Technology Officer |

David F. Beck | | 65 | | Vice President and Controller |

Marcy L. Campbell | | 54 | | Vice President, Human Resources |

Brian J. Dunn | | 60 | | Executive Vice President, Strategy and Corporate Development |

Steven D. Gackenbach | | 54 | | Group President, Memorialization |

Robert M. Marsh | | 49 | | Vice President and Treasurer |

Steven F. Nicola | | 57 | | Chief Financial Officer and Secretary |

Paul F. Rahill | | 60 | | President, Environmental Solutions Division |

David A. Schawk | | 61 | | Group President, SGK Brand Solutions |

Brian D. Walters | | 48 | | Vice President and General Counsel |

Joseph C. Bartolacci was appointed President and Chief Executive Officer effective October 2006.

Gregory S. Babe was appointed Chief Technology Officer effective November 2015. Prior thereto he had been the interim Executive Vice President, Global Information Technology and Integration since November 2014 when he joined the Company. Prior to joining the Company, Mr. Babe was the President and Chief Executive Officer of Liquid X Printed Metals, Inc., from June 2013 to November 2014 and Chief Executive Officer of Orbital Engineering, Inc., from July 2012 to June 2013.

David F. Beck was appointed Vice President and Controller effective February 2010.

Marcy L. Campbell was appointed Vice President, Human Resources effective November 2014. Ms. Campbell served as Director, Regional Human Resources from January 2013, and as Manager, Regional Human Resources from November 2005 to December 2012.

Brian J. Dunn was appointed Executive Vice President, Strategy and Corporate Development effective July 2014. Prior thereto, he served as Group President, Brand Solutions since February 2010.

Steven D. Gackenbach was appointed Group President, Memorialization effective October 31, 2011.

Robert M. Marsh was appointed Vice President and Treasurer in February 2016. He served as Treasurer since December 2014 when he joined the Company. Prior to joining the Company, Mr. Marsh was a partner of PNC Mezzanine Capital, the principal mezzanine investment business of The PNC Financial Services Group, LLC ("PNC"). Mr. Marsh joined PNC in 1997.

Steven F. Nicola was appointed Chief Financial Officer and Secretary effective December 2003.

Paul F. Rahill was appointed President, Environmental Solutions Division in October 2002.

David A. Schawk joined the Company in July 2014 as President, SGK Brand Solutions upon Matthews' acquisition of Schawk. Mr. Schawk served as Schawk's Chief Executive Officer from July 2012 and was a member of the Schawk Board of Directors since 1992.

Brian D. Walters was appointed Vice President and General Counsel effective February 2009.

ITEM 5. MARKET FOR REGISTRANT'S COMMON EQUITY AND RELATED STOCKHOLDER MATTERS.

Market Information:

The authorized common stock of the Company consists of 70,000,000 shares of Class A Common Stock, $1.00 par value. At September 30, 2017, 32,148,579 shares were outstanding. The Company's Class A Common Stock is traded on the NASDAQ Global Select Market under the symbol "MATW". The following table sets forth the high, low and closing prices as reported by Nasdaq for the periods indicated:

|

| | | | | | | | | | | |

| High | | Low | | Close |

Fiscal 2017: | | | | | |

Quarter ended: September 30, 2017 | $ | 66.65 |

| | $ | 57.40 |

| | $ | 62.25 |

|

June 30, 2017 | 72.60 |

| | 60.40 |

| | 61.25 |

|

March 31, 2017 | 77.85 |

| | 64.45 |

| | 67.65 |

|

December 31, 2016 | 77.10 |

| | 57.65 |

| | 76.85 |

|

Fiscal 2016: | | | | | |

Quarter ended: September 30, 2016 | $ | 62.85 |

| | $ | 54.76 |

| | $ | 60.76 |

|

June 30, 2016 | 56.05 |

| | 49.37 |

| | 55.64 |

|

March 31, 2016 | 54.80 |

| | 45.00 |

| | 51.47 |

|

December 31, 2015 | 61.10 |

| | 46.05 |

| | 53.45 |

|

The Company has a stock repurchase program. The buy-back program is designed to increase shareholder value, enlarge the Company's holdings of its common stock, and add to earnings per share. Repurchased shares may be retained in treasury, utilized for acquisitions, or reissued to employees or other purchasers, subject to the restrictions of the Company's Restated Articles of Incorporation. Under the current authorization, the Company's Board of Directors has authorized the repurchase of a total of 5,000,000 shares of Matthews' common stock under the program, of which 1,816,146 shares remain available for repurchase as of September 30, 2017. All purchases of the Company's common stock during fiscal 2017 were part of this repurchase program.

In May 2016, the Company purchased 970,000 common shares under the buy-back program from members of the Schawk family, including David A. Schawk (who is a member of the Board of Directors of the Company and the Company's President, SGK Brand Solutions) and certain family members of Mr. Schawk and/or trusts established for the benefit of Mr. Schawk or his family members. The purchase price for the shares purchase was $50.6921625 per share, which was equal to 96.76% of the average of the high and low trading prices for the common stock as reported on the Nasdaq Global Select Market on May 12, 2016.

ITEM 5. MARKET FOR REGISTRANT'S COMMON EQUITY AND RELATED STOCKHOLDER MATTERS, (continued)

The following table shows the monthly fiscal 2017 stock repurchase activity:

|

| | | | | | | | | | | | | |

Period | | Total number of shares purchased | | Weighted-average price paid per share | | Total number of shares purchased as part of a publicly announced plan | | Maximum number of shares that may yet be purchased under the plan |

October 2016 | | — |

| | $ | — |

| | — |

| | 2,028,570 |

|

November 2016 | | 83,293 |

| | 67.49 |

| | 83,293 |

| | 1,945,277 |

|

December 2016 | | 11,936 |

| | 73.63 |

| | 11,936 |

| | 1,933,341 |

|

January 2017 | | — |

| | — |

| | — |

| | 1,933,341 |

|

February 2017 | | 39,918 |

| | 66.98 |

| | 39,918 |

| | 1,893,423 |

|

March 2017 | | — |

| | — |

| | — |

| | 1,893,423 |

|

April 2017 | | 126 |

| | 67.66 |

| | 126 |

| | 1,893,297 |

|

May 2017 | | 38,499 |

| | 63.70 |

| | 38,499 |

| | 1,854,798 |

|

June 2017 | | 260 |

| | 62.55 |

| | 260 |

| | 1,854,538 |

|

July 2017 | | 5,500 |

| | 65.60 |

| | 5,500 |

| | 1,849,038 |

|

August 2017 | | 13,666 |

| | 65.45 |

| | 13,666 |

| | 1,835,372 |

|

September 2017 | | 19,226 |

| | 58.22 |

| | 19,226 |

| | 1,816,146 |

|

Total | | 212,424 |

| | $ | 66.03 |

| | 212,424 |

| | |

|

Holders:

Based on records available to the Company, the number of record holders of the Company's common stock was 611 at October 31, 2017.

Dividends:

A quarterly dividend of $0.19 per share was declared to shareholders of record on November 16, 2017. The Company paid quarterly dividends of $0.17, $0.15, and $0.13 per share for each of the quarters during fiscal 2017, 2016, and 2015, respectively.

Cash dividends have been paid on common shares in every year for at least the past forty-eight years. It is the present intention of the Company to continue to pay quarterly cash dividends on its common stock. However, there is no assurance that dividends will be declared and paid as the declaration and payment of dividends is at the discretion of the Board of Directors of the Company and is dependent upon many factors, including but not limited to the Company's financial condition, results of operations, cash requirements, future prospects and other factors deemed relevant by the Board.

Securities Authorized for Issuance Under Equity Compensation Plans:

See Equity Compensation Plans in Item 12 "Security Ownership of Certain Beneficial Owners and Management" on page 77 of this report.

ITEM 5. MARKET FOR REGISTRANT'S COMMON EQUITY AND RELATED STOCKHOLDER MATTERS, (continued)

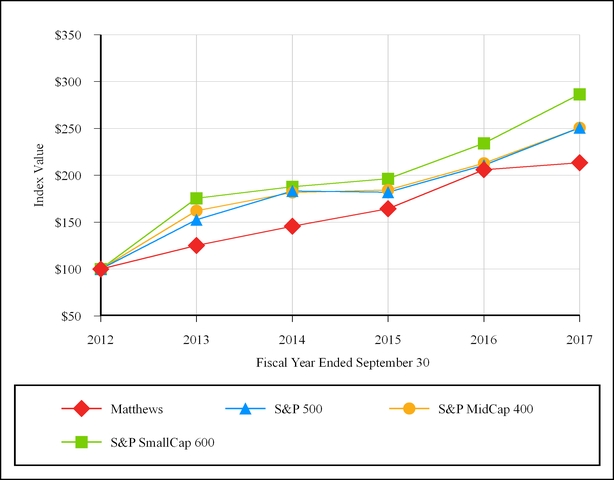

PERFORMANCE GRAPH

COMPARISON OF FIVE-YEAR CUMULATIVE RETURN *

AMONG MATTHEWS INTERNATIONAL CORPORATION,

S&P 500 INDEX, S&P MIDCAP 400 INDEX AND S&P SMALLCAP 600 INDEX

* Total return assumes dividend reinvestment

Note: Performance graph assumes $100 invested on October 1, 2012 in Matthews International Corporation Common Stock, Standard & Poor's (S&P) 500 Index, S&P MidCap 400 Index and S&P SmallCap 600 Index. The results are not necessarily indicative of future performance.

ITEM 6. SELECTED FINANCIAL DATA.

|

| | | | | | | | | | | | | | | | | | | |

| Years Ended September 30, |

| 2017(1) | | 2016(2) | | 2015(3) | | 2014(4) | | 2013(5) |

| (Amounts in thousands, except per share data) (Unaudited) |

Net sales | $ | 1,515,608 |

| | $ | 1,480,464 |

| | $ | 1,426,068 |

| | $ | 1,106,597 |

| | $ | 985,357 |

|

| | | | | | | | | |

Operating profit | 112,603 |

| | 118,815 |

| | 105,023 |

| | 81,522 |

| | 94,615 |

|

| | | | | | | | | |

Interest expense | 26,371 |

| | 24,344 |

| | 20,610 |

| | 12,628 |

| | 12,925 |

|

| | | | | | | | | |

Net income attributable to Matthews shareholders | $ | 74,368 |

| | $ | 66,749 |

| | $ | 63,449 |

| | $ | 42,625 |

| | $ | 54,121 |

|

| | | | | | | | | |

Earnings per common share: | | | | | | | | | |

Basic | $ | 2.31 |

| | $ | 2.04 |

| | $ | 1.93 |

| | $ | 1.51 |

| | $ | 1.96 |

|

Diluted | 2.28 |

| | 2.03 |

| | 1.91 |

| | 1.49 |

| | 1.95 |

|

| | | | | | | | | |

Weighted-average common | | | | | | | | | |

shares outstanding: | | | | | | | | | |

Basic | 32,240 |

| | 32,642 |

| | 32,939 |

| | 28,209 |

| | 27,255 |

|

Diluted | 32,570 |

| | 32,904 |

| | 33,196 |

| | 28,483 |

| | 27,423 |

|

| | | | | | | | | |

Cash dividends per share | $ | 0.68 |

| | $ | 0.60 |

| | $ | 0.54 |

| | $ | 0.46 |

| | $ | 0.41 |

|

| | | | | | | | | |

Total assets | $ | 2,244,649 |

| | $ | 2,091,041 |

| | $ | 2,143,611 |

| | $ | 2,008,026 |

| | $ | 1,209,245 |

|

Long-term debt, non-current | 881,602 |

| | 844,807 |

| | 891,217 |

| | 714,027 |

| | 351,068 |

|

| |

(1) | Fiscal 2017 included net pre-tax charges of $38,458 and income of $10,483, which impacted operating profit and other deductions, respectively. These pre-tax charges primarily consisted of acquisition-related costs, and strategic cost-reduction initiatives. The pre-tax income primarily consisted of loss recoveries, net of related costs, related to the previously disclosed theft of funds by a former employee. |

| |

(2) | Fiscal 2016 included net pre-tax charges of $36,057 and income of $78, which impacted operating profit and other deductions, respectively. These amounts primarily consisted of acquisition-related costs and strategic cost-reduction initiatives. |

| |

(3) | Fiscal 2015 included pre-tax charges of $36,883 and income of $8,726, which impacted operating profit and other deductions, respectively, and also included the unfavorable effect of related adjustments of $1,334 to income tax expense. These amounts primarily consisted of acquisition-related costs, trade name write-offs, strategic cost-reduction initiatives, and losses related to a theft of funds, partially offset by a gain on the settlement of a multi-employer pension plan obligation, and the impact of the favorable settlement of litigation, net of related expenses. |

| |

(4) | Fiscal 2014 included net pre-tax charges of approximately $41,289, primarily related to acquisition-related costs, strategic cost-reduction initiatives, and litigation expenses related to a legal dispute in the Memorialization segment. Charges of $38,598 and $2,691 impacted operating profit and other deductions, respectively. In addition, fiscal 2014 included the unfavorable effect of adjustments of $1,347 to income tax expense related to non-deductible expenses related to acquisition activities. |

| |

(5) | Fiscal 2013 included net pre-tax charges of approximately $15,352, which primarily related to strategic cost-reduction initiatives, incremental costs related to an ERP implementation in the Memorialization segment, acquisition-related costs and an impairment charge related to the carrying value of a trade name. The charges were partially offset by a gain on the final settlement of the purchase price of the remaining ownership interest in one of the Company's subsidiaries and the benefit of adjustments to contingent consideration. |

ITEM 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS.

The following discussion should be read in conjunction with the consolidated financial statements of Matthews and related notes thereto. In addition, see "Cautionary Statement Regarding Forward-Looking Information" included in Part I of this Annual Report on Form 10-K.

RESULTS OF OPERATIONS:

The following table sets forth sales and operating profit for the Company's SGK Brand Solutions, Memorialization and Industrial Technologies segments for each of the last three fiscal years.

|

| | | | | | | | | | | |

| Years Ended September 30, |

| 2017 | | 2016 | | 2015 |

| (Dollars in thousands) |

Sales to unaffiliated customers: | | | | | |

SGK Brand Solutions | $ | 770,181 |

| | $ | 755,975 |

| | $ | 798,339 |

|

Memorialization | 615,882 |

| | 610,142 |

| | 508,058 |

|

Industrial Technologies | 129,545 |

| | 114,347 |

| | 119,671 |

|

Consolidated | $ | 1,515,608 |

| | $ | 1,480,464 |

| | $ | 1,426,068 |

|

| | | | | |

Operating Profit: | | | | | |

SGK Brand Solutions | $ | 24,919 |

| | $ | 42,909 |

| | $ | 21,864 |

|

Memorialization | 80,652 |

| | 68,252 |

| | 70,064 |

|

Industrial Technologies | 7,032 |

| | 7,654 |

| | 13,095 |

|

Consolidated | $ | 112,603 |

| | $ | 118,815 |

| | $ | 105,023 |

|

Comparison of Fiscal 2017 and Fiscal 2016:

Sales for the year ended September 30, 2017 were $1.52 billion, compared to $1.48 billion for the year ended September 30, 2016. The increase in fiscal 2017 sales of $35.1 million principally reflected higher sales of cemetery memorial products and cremation equipment, increased sales in the U.K. and Asia Pacific brand markets, higher sales of marking products, and the benefits from recently completed acquisitions (see "Acquisitions" below). These increases were partially offset by slower market conditions in North America and Europe for the SGK Brand Solutions segment, lower unit sales of caskets, and the unfavorable impact of changes in foreign currencies against the U.S. dollar of $12.8 million compared to a year ago.

In the SGK Brand Solutions segment, sales for fiscal 2017 were $770.2 million, compared to $756.0 million in fiscal 2016. The increase in sales reflected sales growth in the U.K. and Asia Pacific markets, and the completion of three acquisitions during the second quarter of fiscal 2017. These sales increases were partially offset by slower brand market conditions in the U.S. and Europe, and the unfavorable impact of changes in foreign currency values against the U.S. dollar of approximately $12.1 million. Memorialization segment sales for fiscal 2017 were $615.9 million compared to $610.1 million for fiscal 2016. The sales increase reflected higher sales of cemetery memorial products and cremation equipment, partially offset by lower unit sales of caskets (reflecting an estimated decline in U.S. casketed deaths). Industrial Technologies segment sales for fiscal 2017 were $129.5 million, compared to $114.3 million for fiscal 2016. The increase reflected higher sales of marking products and OEM solutions, and the favorable impact of recently completed acquisitions, partially offset by lower sales of fulfillment systems and the unfavorable impact of changes in foreign currency values against the U.S. dollar of approximately $690,000.

ITEM 7. MANAGEMENT'S DISCUSSION AND ANALYSIS, (continued)

Gross profit for the year ended September 30, 2017 was $563.4 million, compared to $556.5 million for fiscal 2016. The increase in gross profit primarily reflected the impact of higher sales from recent acquisitions, the benefits of productivity initiatives, and realization of acquisition synergies, partially offset by unfavorable changes in foreign currency values against the U.S. dollar, and slower market conditions in North America and Europe for the SGK Brand Solutions segment. Fiscal 2017 gross profit also included an expense of $2.0 million for the write-off of inventory step-up value related to the current year acquisitions. Fiscal 2016 gross profit included an expense of approximately $4.0 million for the partial write-off of inventory step-up value related to the acquisition of Aurora Products Group, LLC ("Aurora") in August 2015.

Selling and administrative expenses for the year ended September 30, 2017 were $450.8 million, compared to $437.6 million for fiscal 2016. Consolidated selling and administrative expenses as a percent of sales were 29.7% for fiscal 2017, compared to 29.6% in fiscal 2016. The increase in selling and administrative expenses reflected the impact of recently completed acquisitions, partially offset by the benefits from cost-reduction initiatives, including acquisition integration synergies. Selling and administrative expenses in fiscal 2017 also included an increase of $3.7 million in intangible asset amortization related to recently completed acquisitions, and $3.3 million of incremental stock-based compensation expense that was recognized in the first fiscal quarter of fiscal 2017 as a result of required accounting treatment for retirement-eligible employees. Selling and administrative expenses also included acquisition integration and related systems-integration costs, and other charges in connection with cost structure initiatives totaling $35.2 million in fiscal 2017, compared to $32.1 million in fiscal 2016.

Operating profit for fiscal 2017 was $112.6 million, compared to $118.8 million for fiscal 2016. The SGK Brand Solutions segment operating profit for fiscal 2017 was $24.9 million, compared to $42.9 million for fiscal 2016. Fiscal 2017 operating profit for the SGK Brand Solutions segment included acquisition integration costs and other charges totaling $29.7 million, compared to $25.0 million in fiscal 2016. Segment operating profit in fiscal 2017 also included an increase of $3.1 million in intangible asset amortization related to recently completed acquisitions. Additionally, fiscal 2017 operating profit for SGK Brand Solutions reflected slower market conditions in North America and Europe, and the unfavorable impact of changes in foreign currencies against the U.S. dollar of approximately $1.3 million, partially offset by the favorable impact of recent acquisitions. Memorialization segment operating profit for fiscal 2017 was $80.7 million, compared to $68.3 million for fiscal 2016. The increase in segment operating profit reflected higher cemetery memorial and cremation equipment sales, and the benefits of acquisition synergies and other productivity initiatives, partially offset by the impact of lower casket sales. Fiscal 2017 operating profit for the Memorialization segment also included acquisition integration costs and other charges totaling $7.8 million, compared to $10.4 million in fiscal 2016. Operating profit for the Industrial Technologies segment for fiscal 2017 was $7.0 million, compared to $7.7 million in fiscal 2016. The benefits of higher sales were offset by higher investments in the segment's product development, and an increase in acquisition related charge.